March 3, 2026

Understanding Capacity Price Risk in PJM: Navigating the 2026–2027 Market Shift

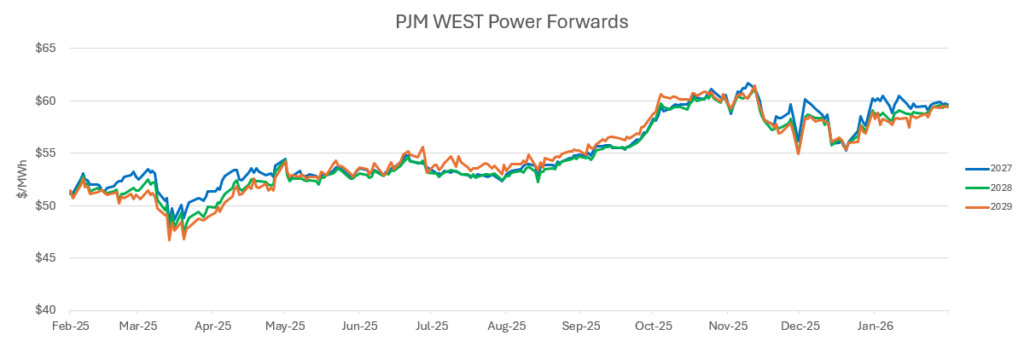

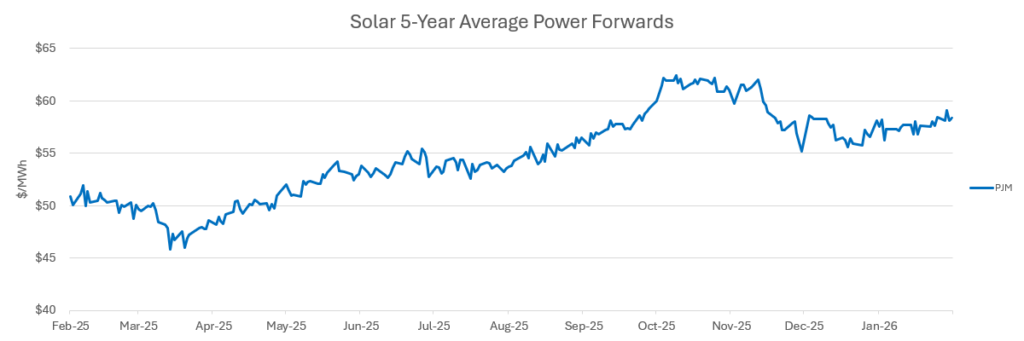

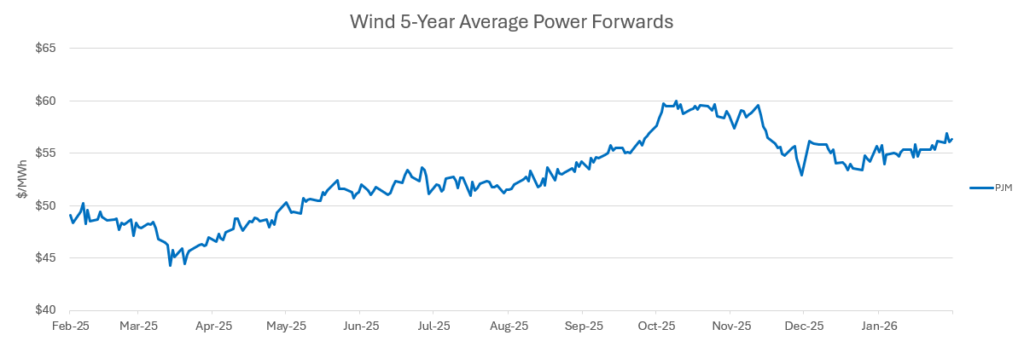

PJM capacity prices are in a sustained high-cost phase driven by demand growth and tightening supply, with potentially meaningful bill impacts.

- The FERC mandated compliance filing related to co-located loads was filed by PJM on February 23rd. PJM continues to evaluate programs that will adequately deal with this contentious issue.

- Additionally, FERC had previously asked PJM to file a brief and respond to specific questions on the establishment of new transmission rates, which are also related to the co-location issue.

- The DOE utilized provisions under the Federal Power Act to direct Constellation to do whatever is necessary to ensure that Eddystone Units 3 and 4 remained operational through May/2026.

NYISO Regulatory Review

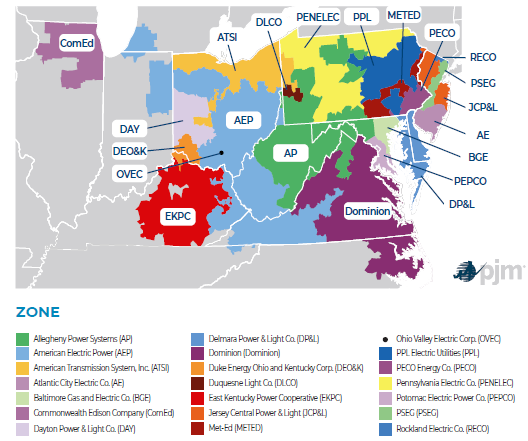

- The NYISO continues to review the conditions and operational impacts during the duration of the cold event that occurred in January.

- The major load centers in Zones F-K are still reliant on fossil generation, with behind-the-meter solar (~ 6GW) contributing very little due to overcast conditions, and system operators depend on oil generation to manage through the peaks.

Market Drivers

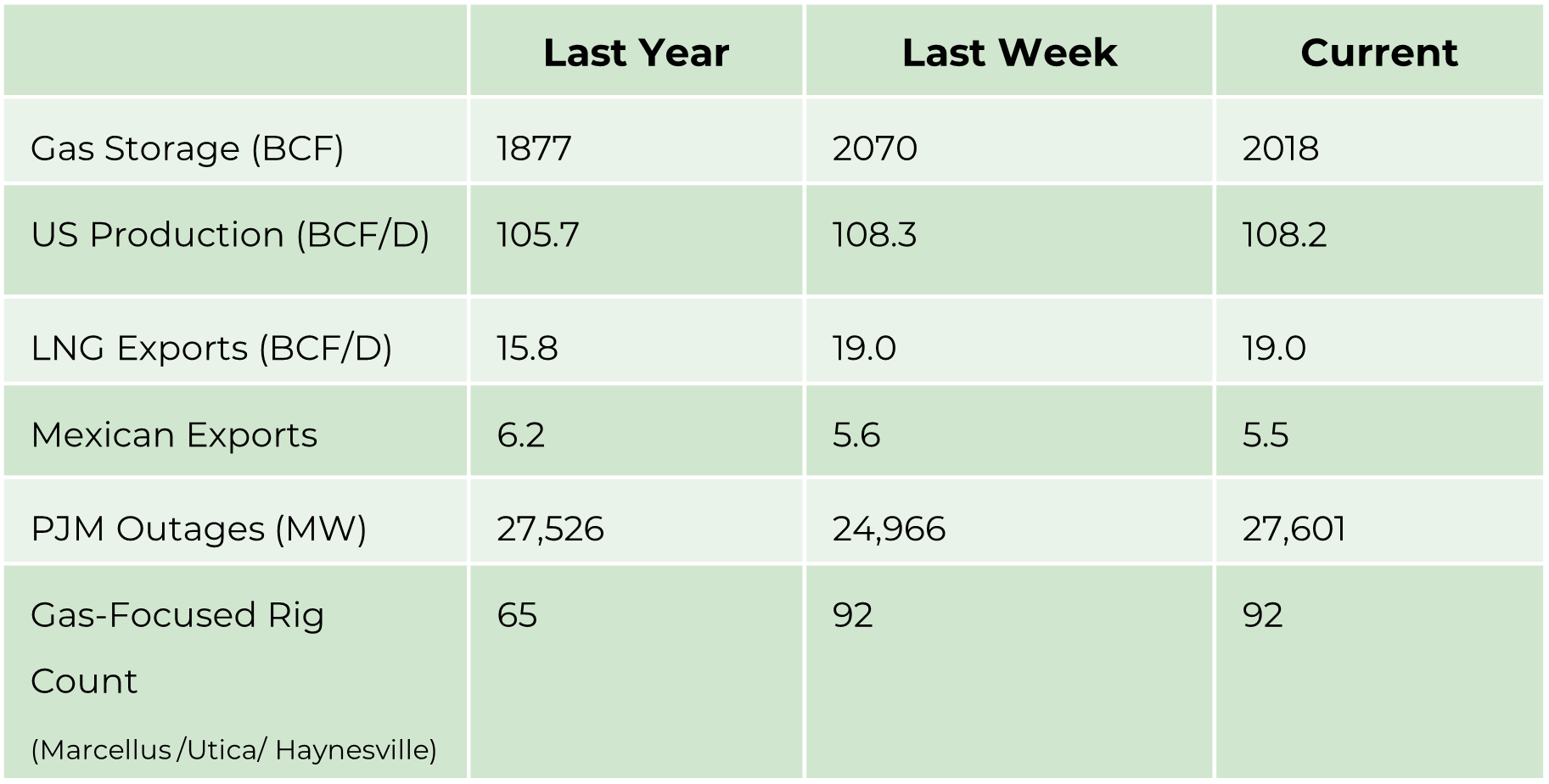

- Gas Storage/Year over year difference. A positive number is bearish, and a negative number is bullish.

- Production /Year over year growth/trend is important in the context of demand growth.

- LNG Exports/Year over year growth means demand is growing and should be looked at in comparison to production trend.

- Mexican Exports/Add to LNG Exports to show a trend in exports compared to the production trend.

- PJM Outages- generally seasonal in Spring or Fall/Can support short-term prices.

- Gas Focused Rig Count/Is drilling increasing to grow production versus demand growth. This can be seen as impacting price in the future based on expected load growth.

Energy Market Update

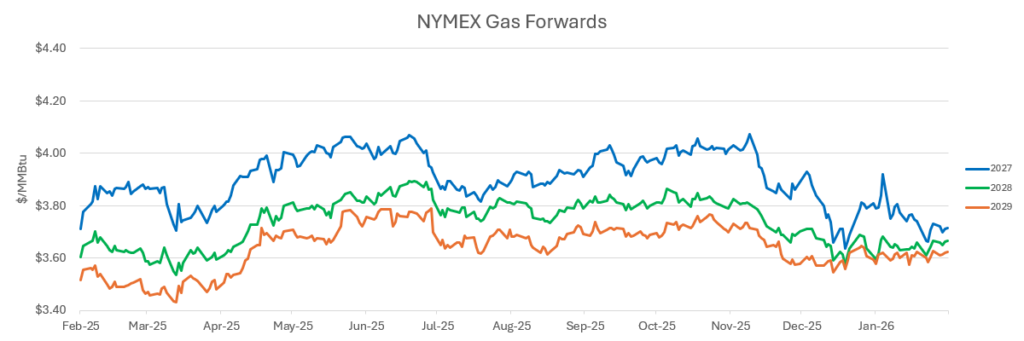

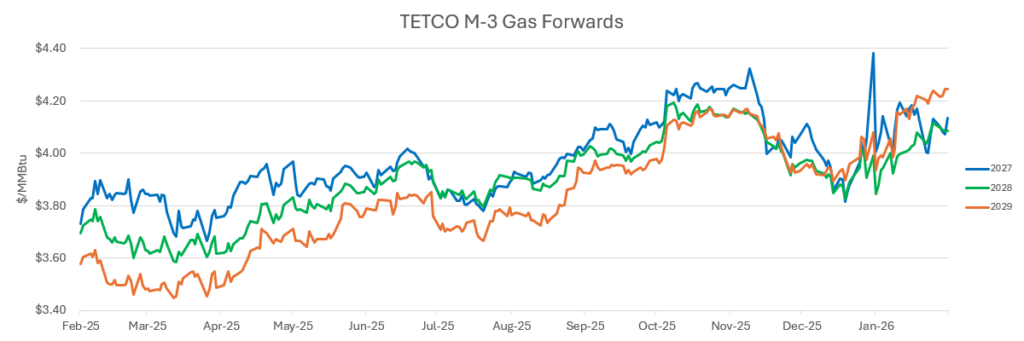

- The volatility of the weather is reflected in the withdrawal figures reported weekly by EIA. From a record 360 BCF withdrawal reported several weeks ago to the March 1st paltry 52 BC drawdown puts end-of-season inventories at comfortable levels within the 5-year average.

- Given the current weather forecast, the market could see an early start to the injection season with the turn around from withdrawals to injections coming by the 3rd week of March.

- Permitting reform and load forecasting accuracy continue to be hot topics in PJM and other ISO’s experiencing rapid, large load growth from data centers. Hyper-scalers are motivated to support and/or recommend methodological modifications in order to expedite the deployment of new dispatchable generation while the governing bodies remain concerned about reliability and costs.

- LNG exports have returned to pre-Fern levels after an almost 6 BCF/D cut during the peak of the cold. Those export cuts helped support the grid as domestic gas prices escalated to factors above global LNG prices and acted as virtual storage.

- Continued cold in Europe has supported rapid withdrawals from storage and left inventories at record lows, with more cold weather expected. Roughly 80% of US LNG exports have been heading to Europe, which will continue through the summer’s re-fill season.