June 15, 2026

What Businesses Need to Know: Insights from Our Summer 2026 Energy Outlook Webinar

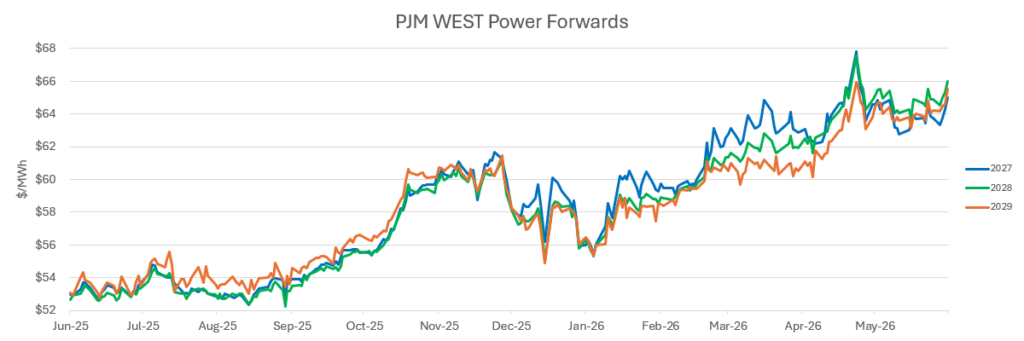

- PJM continues to review the April 27 submissions (estimated at 200,000 MW) from developers outlining potential projects for selection in the September supplemental capacity auction, as the ISO works to close the capacity shortfall from prior auctions.

- PJM plans to acquire the capacity shortfall and award long-term contracts to support the development of resources that can be available by June of 2031. This requirement will be a difficult hurdle for many of the projects submitted, given the current development timeline, turbine availability, and supply chain issues.

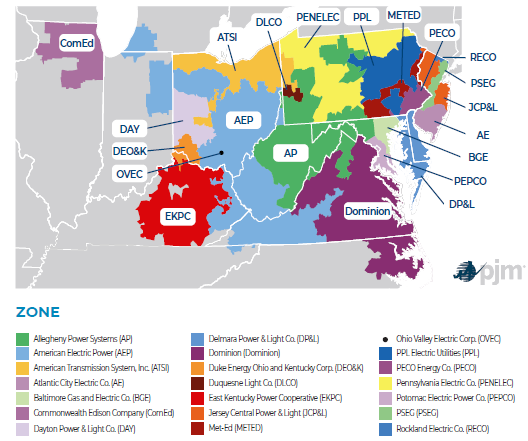

- PJM formally asked Talen to extend the current Reliability Must Run (RMR) contracts for Wagner and Brandon Shores as BG&E continues to be a challenging load zone to serve.

- Regulators continue to scrutinize PJM’s operations in light of escalating costs and dissatisfaction with capacity management.

NYISO Regulatory Review

- The New York assembly is considering whether a one-year ban a new data centers would be appropriate given the overall generation situation and tightness in the market. New interconnect requests totals near 12,000 MW which without new dispatchable generation would only further tighten reserve margins.

- The Champlain Hudson Power Express (CHPE) has started to deliver power to New York after the 339-mile line costing upwards of $6 billion was recently energized. Designed to deliver 1250 MW into New York City, the added deliveries into the grid should help slow the ascent of power and capacity prices.

- The state of New York announced a moratorium on data center construction for at least one year while it assesses its current supply/demand imbalance.

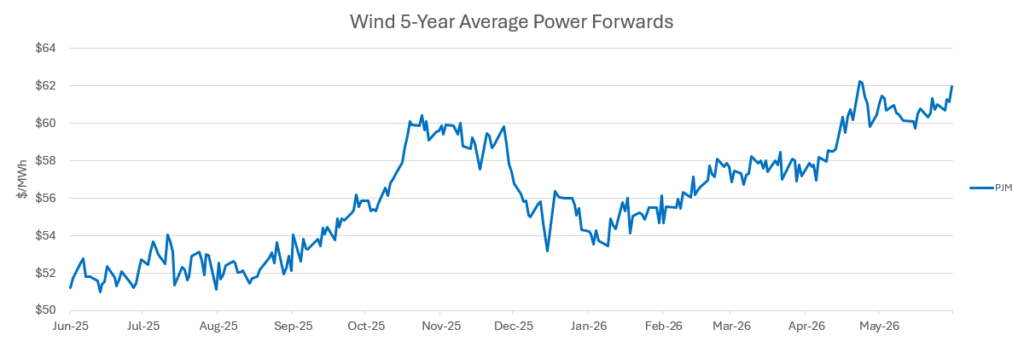

Market Drivers

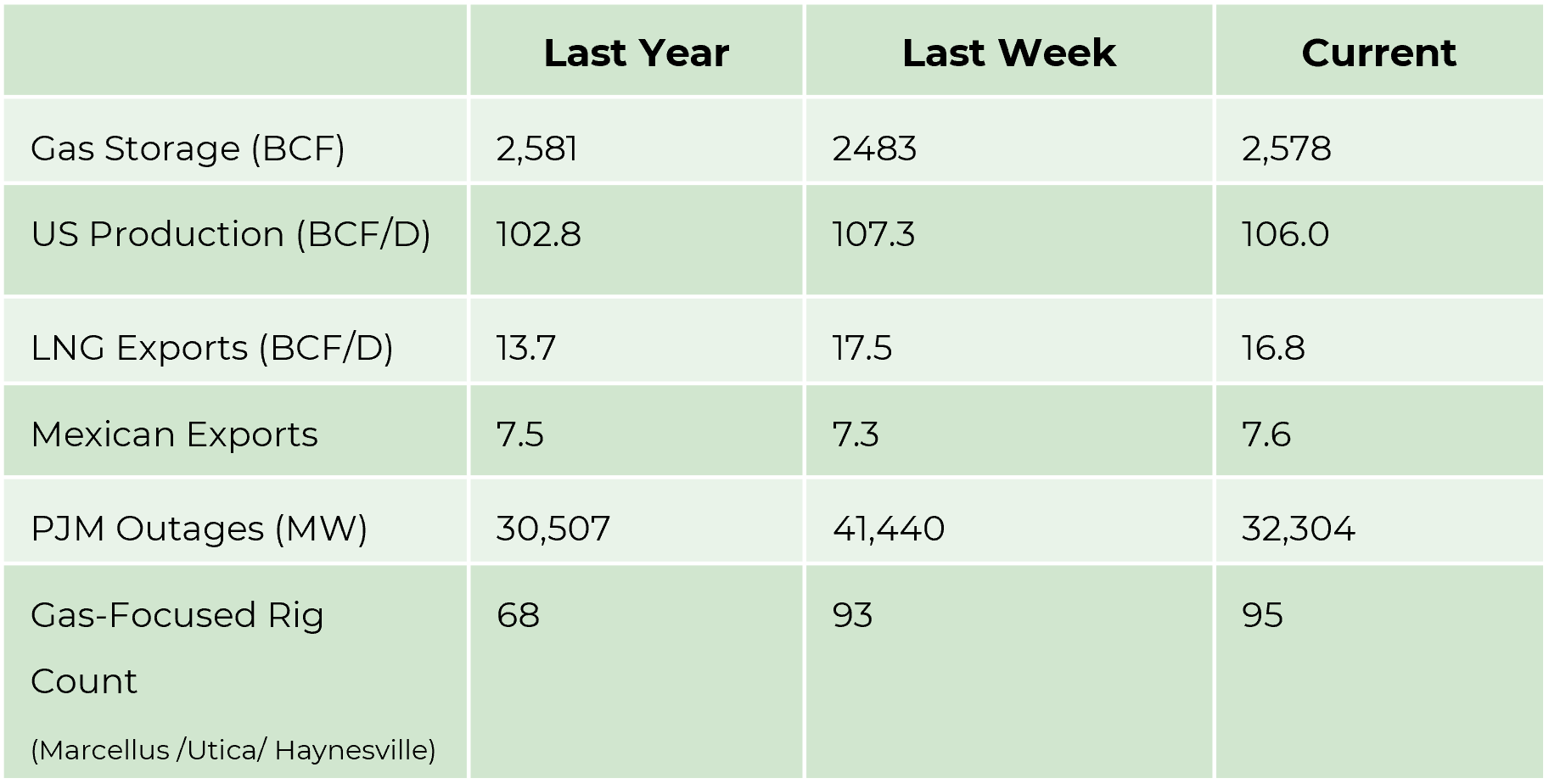

Market Drivers as of June 9, 2026.

- Gas Storage/Year over year difference. A positive number is bearish, and a negative number is bullish.

- Production /Year over year growth/trend is important in the context of demand growth.

- LNG Exports/Year over year growth means demand is growing and should be looked at in comparison to production trend.

- Mexican Exports/Add to LNG Exports to show a trend in exports compared to the production trend.

- PJM Outages- generally seasonal in Spring or Fall/Can support short-term prices.

- Gas Focused Rig Count/Is drilling increasing to grow production versus demand growth. This can be seen as impacting price in the future based on expected load growth.

Energy Market Update

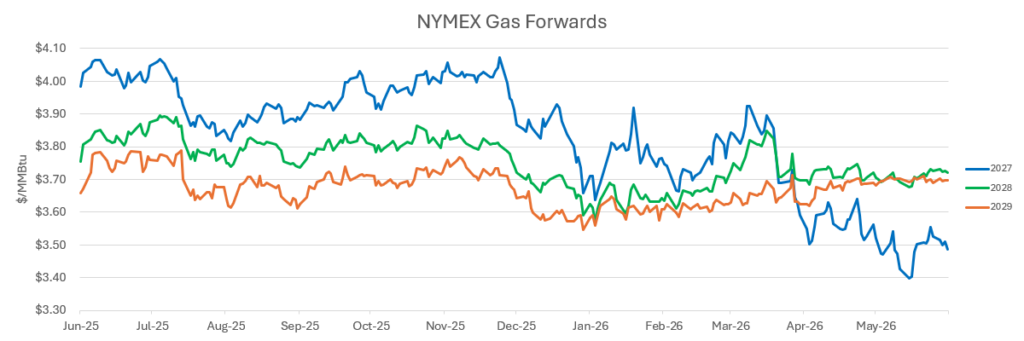

- Benign weather throughout most of the East Coast has kept cash prices for natural gas straddling the $2.00/MMBTU area, while the July NYMEX contract has seen dip buyers become aggressive. Strategic buyers have also scaled into Calendar/2027, which momentarily was on sale under $3.50/MMBTU and traded down to $3.37 before the blinking neon sign appeared and offers started getting lifted.

- US LNG export terminals performing seasonal maintenance have reduced exports by about 2 BCF/D while US production has stayed between 106 BCF/D and 108 BCF/D. This has allowed the storage comparisons to trend bullishly with the year-over-year comparison now flat (2578 versus 2581).

- Oil prices traded below $90/Barrel for a brief time last week. A juggernaut of oil and product exports out of the US has eased the physical market stress for the short term, but the current level of inventory withdrawals is not sustainable.