August 4, 2025

An Analysis of the 2026/2027 pJM Base Residual auction Results

Following the recent release of the PJM BRA Results for 2026/2027, CPV Retail held a webinar to provide a detailed analysis of the outcomes and the factors that led to these results. Below is a brief summary of the key points discussed during the session.

Following the recent release of the PJM BRA Results for 2026/2027, CPV Retail held a webinar to provide a detailed analysis of the outcomes and the factors that led to these results. Below is a brief summary of the key points discussed during the session. For additional insights, be sure to check out the webinar, now available on-demand, featuring Khristian Camacho, Vice President of Pricing and Supply at CPV Retail, and Dan Jerke, Vice President of Energy Management at CPV.

How We Got Here:

As we look at the current state of the capacity market, it’s clear we’ve entered a period of tightening — and not by accident.

Over the past year, forecasted demand has risen by 5 gigawatts, signaling a significant uptick in expected load. At the same time, the supply side has underperformed: gains from new renewable resources and delayed retirements didn’t meet expectations. The market was simply short.

As a result, the most recent Base Residual Auction cleared at the price cap of $329.17. Without that cap in place, it would have gone even higher — over $388 per megawatt-day. That tells us just how stressed the market has become.

Each BRA only secures resources for a single delivery year, and because of regulatory delays, these auctions aren’t held with much lead time. Instead of planning several years in advance, we’re often reacting with just a one-year horizon. That limited visibility makes long-term strategy difficult and forces market participants into short-term responses.

We’re already seeing the effects. The cost implications of last year’s auction are now tangible. We’ve entered the delivery period that was secured under those tight market conditions, and the financial impacts are being felt — especially by end users.

EXAMINING THE 2026/2027 RESULTS:

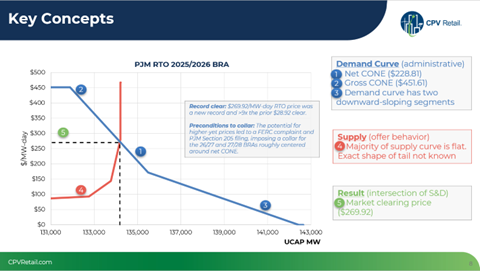

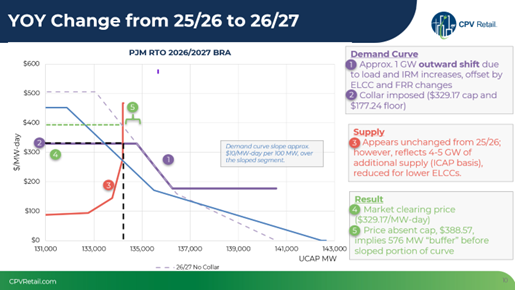

To interpret the results from the BRA, Dan Jerke presented key concepts with a visual of the supply and demand curve in relation to identifying the intersection of supply and demand, which is the market-clearing price.

As mentioned, PJM imposed the price collar, spanning $329 and $177, shown as solid segments, whereas the unconstrained curve is dashed.

Next, supply appears largely unchanged YOY, clearing at a similar level; however, the ELCC adjustment masks the fact that a significant amount of new supply showed up, roughly 4-5 GW across new gen, uprates, and rescinded retirement notices. If you look at the deactivation list, most units have stuck around. Very strong turnout, yet was surpassed by outward shift.

Clearing results at the cap were $329.17. Without the cap, the market would have cleared at $388.57 on the dashed demand curve, according to PJM’s simulation. The slope of this curve is approximately $10 per 100 MW, so a $60 price difference corresponds to a 600 MW buffer before clearing further down the curve. An additional 1% of supply would have moved the market halfway down the sloped segment.

For more insights and a look into what to anticipate for future years, check out the webinar on demand.

PJM Regulatory Review

- The results of the last two capacity auctions have motivated the PJM member states to start reviewing “self-build” options for new gas-fired generation. Many states firmly believe that the capacity auction model is not producing sufficient and timely incentives for the market to bring new capacity online.

- PJM announced the results of the Base Residual Auction (BRA) for the 2027/2028 delivery year with a cleared RTO price of $329.17/MW-day, which is basically at the agreed-to cap negotiated by the Governor of Pennsylvania.

- The DOE announced an emergency order that will allow units at the Wagner Generating Station in Maryland to run beyond normal limits for reliability. The maximum annual hourly limits were put in place due to emissions concerns.

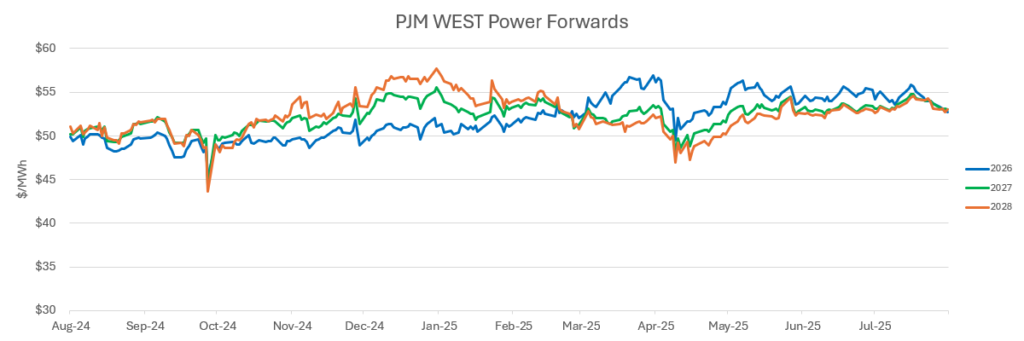

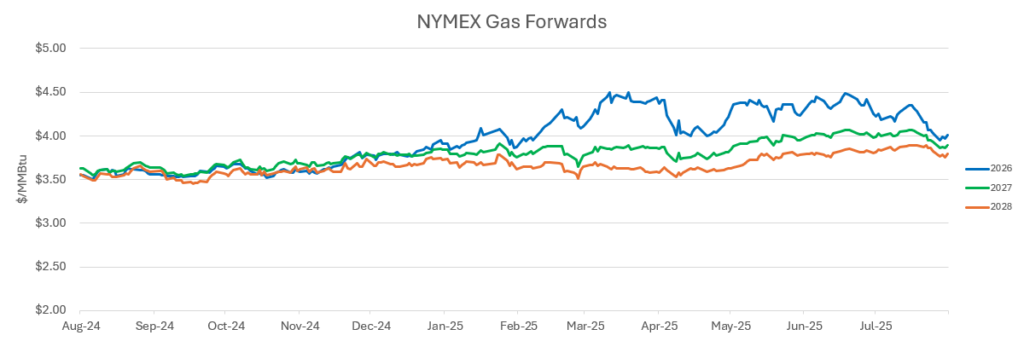

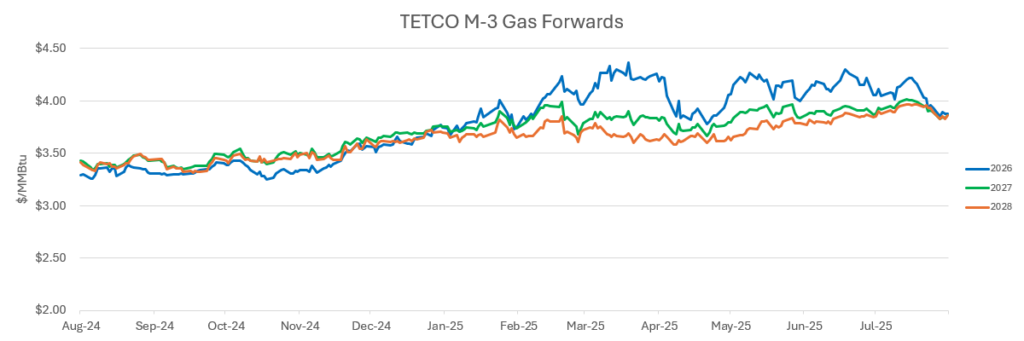

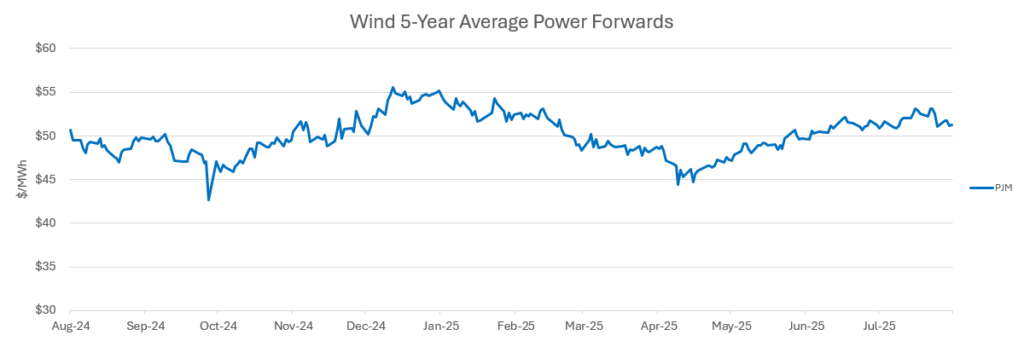

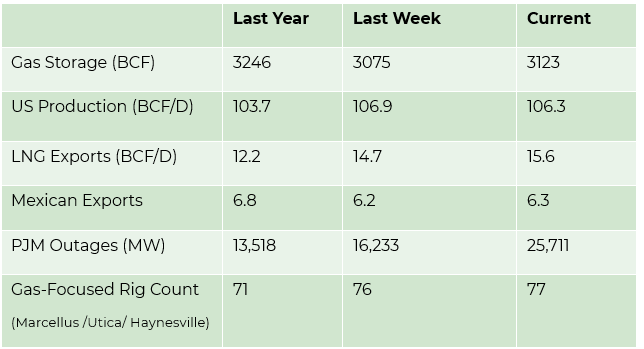

Market Drivers

- Gas Storage/Year over year difference. A positive number is bearish, and a negative number is bullish.

- Production /Year over year growth/trend is important in the context of demand growth.

- LNG Exports/Year over year growth means demand is growing and should be looked at in comparison to production trend.

- Mexican Exports/Add to LNG Exports to show a trend in exports compared to the production trend.

- PJM Outages- generally seasonal in Spring or Fall/Can support short-term prices.

- Gas Focused Rig Count/Is drilling increasing to grow production versus demand growth. This can be seen as impacting price in the future based on expected load growth.

Energy Market Update

- Another heat wave last week concentrated along the population centers in PJM and the southeast induced more volatility into the power markets with day-ahead prices approaching $300/MWH and strong sparks across the grid.

- PJM loads increased and pushed available reserves to extremely low levels as total demand across the footprint exceeded 155,000 MW for several consecutive days, as the ISO went to MaxGen conditions.

- Natural gas-fired generation demand hit a 2025 summer peak last week above 56 BCF/D, with delivered prices in New England exceeding $5.0/MMBTU for several days.

- Strong US production, which averaged close to 107 BCF/D during the recent heat wave, has ensured storage injections remain seasonally elevated and further reduced the differential to last year. Given this pattern, it is expected that total inventories heading into the upcoming winter could exceed last year’s level and possibly reach 4.0 TCF.